Get started for $20/month for 3 months*.

*After 3 months, standard pricing automatically applies

Proven features

Say hello to the way retirement income planning should be. Get turn-by-turn directions as you help clients navigate their way through retirement.

Learn more about Retirement GPS

Proven features

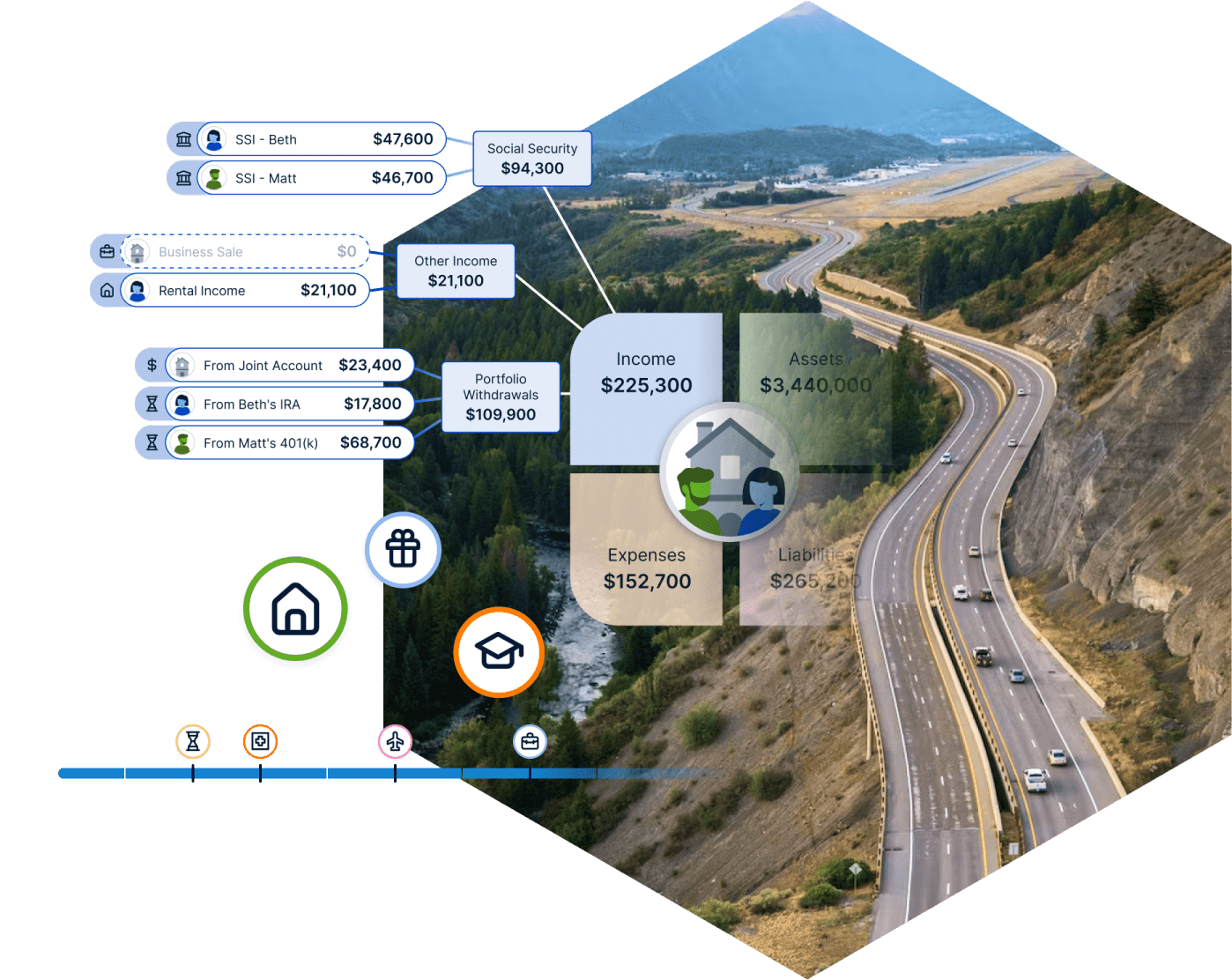

This award-winning interactive view is where all of life's events come together.

Learn more about Life Hub

Proven features

We make tax planning easy. Tax Lab helps you quickly evaluate robust tax strategies in a clear and understandable way, helping you provide valuable advice on portfolio distributions and Roth conversions, down to the account level.

Learn more about Tax Lab

Proven features

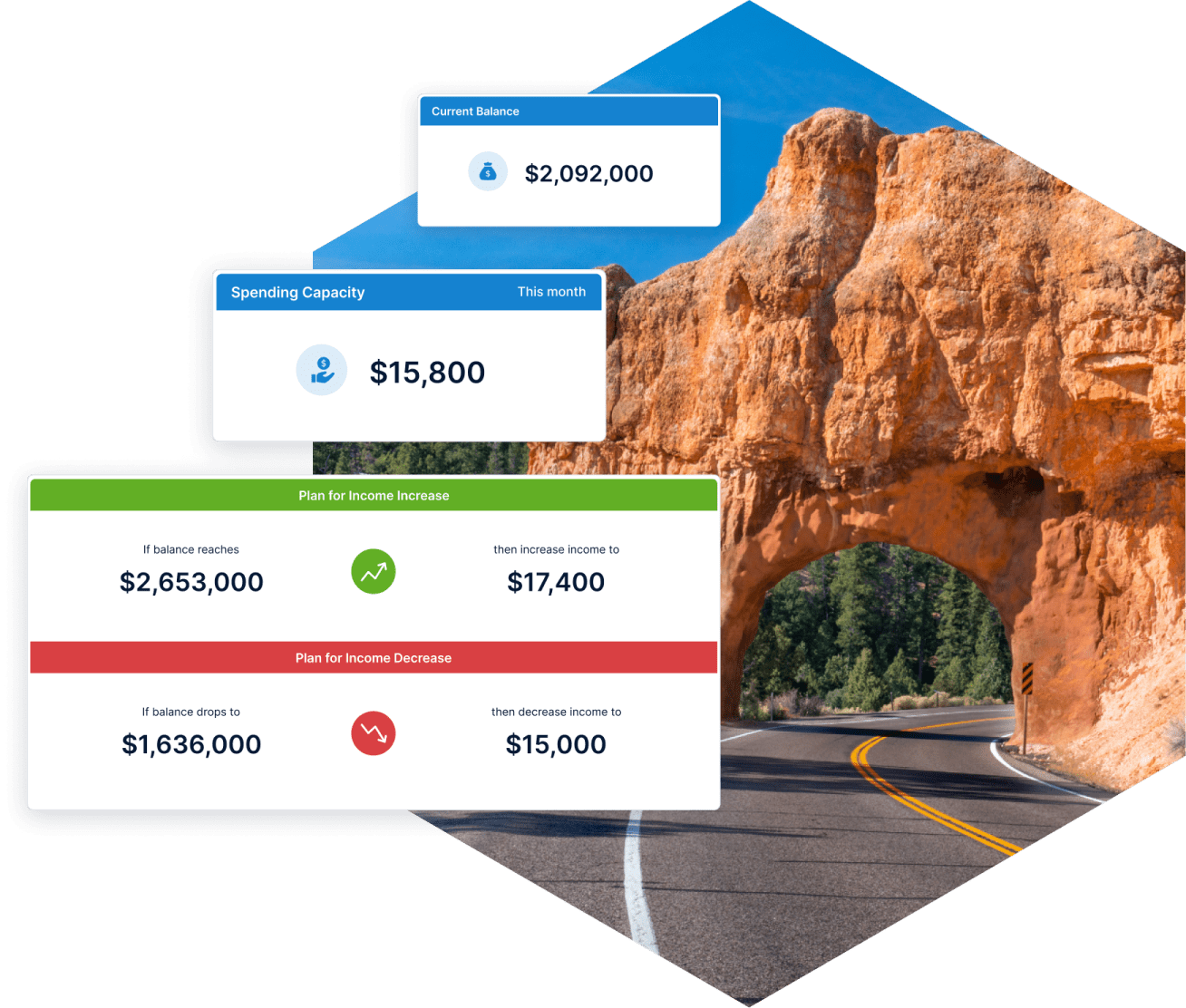

Retirement isn’t pass/fail. With Income Lab's Retirement Stress Test you can see how a plan would navigate some of the most difficult and iconic periods in history.

Learn more about the Retirement Stress Test

Highest advisor value and satisfaction

- Kitces.com 2023 AdvisorTech ReportHighest-Rated Retirement Distribution Planning Tool

- 2023 T3/Inside Information Advisor Software SurveyBest in Show 2022 & 2023

- XYPNLive AdvisorTech ExpoIntegrations make it easy

OUR MISSION

Adjustment-based planning

Clear, confident directions that help clients adapt to a changing world.

Time-saving

Build a plan in minutes, then automate updates and alerts.

Easy to use

Intuitively designed by advisors for advisors.Testimonials

Derek Tharp

“Income Lab has built a tool that provides truly unique insights into retirement income planning that can be implemented with clients in a scalable manner. The team at Income Lab combines good technology, a clear engagement with the retirement income planning research, and a strong business acumen in a way that really excites me about the future of Income Lab and the positive impact Income Lab can have for both advisors and the retirees they serve.”

Miriam Whiteley

“Income Lab has been an important and wonderful addition to my tech stack. Income Lab has helped my worried clients, where percentages didn’t look good enough, see that they are okay in a way that they can understand. It aligned their finances with their decision on when to retire giving them a life of financial freedom from stress and worry.”

Keith Spencer

“Income Lab has been a game changer for me. I’ve used other financial planning software, but one thing that always bothered me is the Monte Carlo probability-of-success percentages. You put in a client’s numbers, and it spits out a probability of success. I’ve always found that to be vague and unsatisfactory, especially when it becomes client-facing. With Income Lab it’s very clear how much you can spend and the guardrails around that number.”

Bob Veres

“Income Lab is the most comprehensive and sophisticated retirement income solution in the current fintech landscape. Not only does it facilitate better, more informed decisions about retirement distribution sufficiency; it also models the various decumulation strategies on an after-tax basis, to help advisors help clients maximize their after-tax retirement income.”